As world leaders gathered in Dubai at the start of COP28 last December, the United Arab Emirates dropped a surprise headline-grabbing announcement. The host nation of the UN talks promised to put $30 billion into a new climate fund aimed at speeding up the energy transition and building climate resilience, especially in the Global South.

ALTÉRRA was billed as the world’s largest private investment vehicle to “focus entirely on climate solutions”. COP28 President Sultan Al-Jaber hailed its launch as “a defining moment” for creating a new era of international climate finance.

Yet four months later, one of the initial funds ALTÉRRA backed with a $300-million commitment agreed to buy a major fossil gas pipeline in North America, Climate Home has discovered.

In March, BlackRock’s “Global Infrastructure Fund IV” acquired half of the 475 km-long Portland Natural Gas Transmission System, with Morgan Stanley taking the rest in a deal worth $1.14 billion overall.

That acquisition would not have come as a surprise to the fund’s investors.

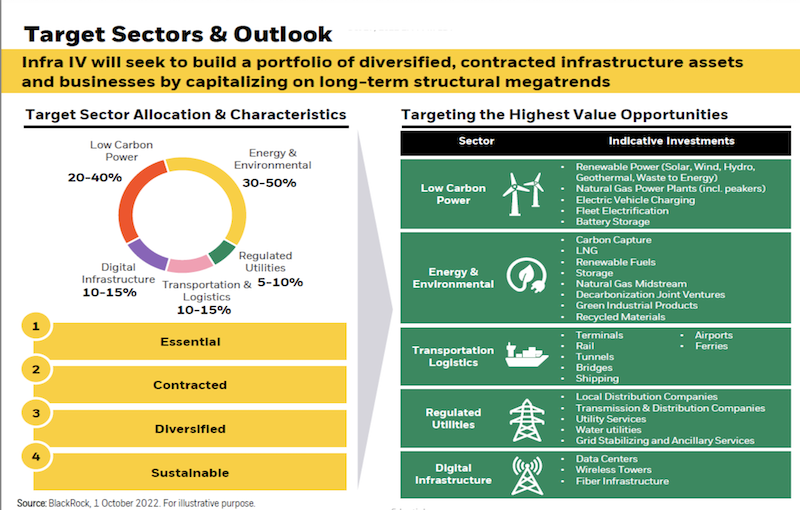

When US-based BlackRock pitched it to the State of Connecticut’s Investment Advisory Council back in 2022, the world’s biggest asset manager gave a flavour of where their money would likely end up. Its presentation – seen by Climate Home – featured a list of “indicative investments” including highly-polluting sectors such as gas power plants and transportation networks, liquefied natural gas (LNG), airports, terminals and shipping.

Climate Home does not know whether ALTÉRRA saw the same presentation, nor did the UAE firm respond directly to a question asking if it was aware before the COP28 announcement that the BlackRock fund might invest in those sectors.

An ALTÉRRA spokesperson told Climate Home its “investments seek to build the energy systems of tomorrow, while supporting the transition of existing energy infrastructure towards a just and managed clean energy ecosystem”.

In addition to the gas pipeline, BlackRock’s infrastructure fund has so far invested in carbon capture, waste management, utilities maintenance services, telecom infrastructure, data centres and the production of industrial gases, according to regulatory filings, a BlackRock job advertisement and press reports accessed by Climate Home.

A BlackRock spokesperson said its global infrastructure fund franchise “targets investments in solutions across the energy transition value chain, driven by the long-term trends of decarbonization, decentralization, and digitalization to support the stability and affordability of energy supply around the world”.

Andreas Sieber, associate director of global policy and campaigns at climate advocacy group 350.org, said Climate Home’s findings “confirm our worst fears”. “The ALTÉRRA fund uses a masquerade of green progress while funnelling investment into fossil fuel pipelines and gas projects, which are the biggest causes of the climate crisis,” he told Climate Home.

Climate finance is a hot topic at UN negotiations, with countries expected to set a new global goal at COP29 in Baku, Azerbaijan, this November, amid persistent calls for higher amounts to help poorer nations boost clean energy production.

The COP28 presidency said last year that ALTÉRRA would “drive forward international efforts to create a fairer climate finance system, with an emphasis on improving access to funding for the Global South”. Al-Jaber added that “its launch reflects… the UAE’s efforts to make climate finance available, accessible and affordable”.

But the sparse details provided at the time prompted climate justice activists to question the real impact it would have in countries that most need financial support to adopt clean energy and adapt to a warming world. Only about a sixth of the fund – $5 billion – was earmarked as “capital to incentivize investment into the Global South”.

Follow the money

ALTÉRRA is a so-called ‘fund of funds’. Instead of directly investing money in individual companies or assets, it puts its cash into a series of funds run by other investment firms. At COP28, it committed a total of $6.5 billion to funds managed by BlackRock, Brookfield and TPG, without setting out how the remaining $23.5 billion would be spent.

Since then, ALTÉRRA has not announced any further investments. Its chief executive, Majid Al Suwaidi, told Bloomberg this month that the fund is “actively planning the next phase of allocations”, without giving further details.

The launch of #ALTÉRRA marks the start of three unique alliances with global asset managers, @Brookfield, @BlackRock, and @tpg.

— ALTÉRRA (@Alterrafund) December 1, 2023

Together, we share the same vision, to bridge the climate investment gap and finance a new climate economy. pic.twitter.com/7yEXOyZqpK

Most of the funds picked by ALTÉRRA remain at an early stage and have yet to announce completed transactions or are still trying to raise more capital from investors. The most notable exception is BlackRock’s fourth Global Infrastructure Fund. By the time it won the $300-million commitment from ALTÉRRA in Dubai, the vehicle was ready to deploy its money.

ALTÉRRA told Climate Home its investment in the BlackRock vehicle is in line with its goals of getting climate finance “flowing quickly and at scale” and of partnering “with funds that invest in the energy transition and accelerate pathways to net-zero”.

Announcing its first $4.5-billion closing in October 2022, BlackRock said the fund would “continue to target investments in climate solutions, while also supporting the infrastructure needed to ensure a stable, affordable energy supply during the transition”.

In private conversations with potential investors, the asset manager spelled out more clearly what that meant.

Its presentation to the State of Connecticut in December 2022 showed that the fund would not only invest in things like renewable energy, electrification and battery storage, but also in fossil gas power plants and pipelines, LNG and transportation infrastructure like airports, shipping and terminals.

A slide from BlackRock’s presentation of the Global Infrastructure Fund IV to investors

In line with this strategy, BlackRock agreed a deal this March for its Global Infrastructure Fund IV to acquire half of the Portland Natural Gas Transmission System (PNGT), a fossil gas pipeline stretching from the Canadian border across New England in the United States to Maine and Massachusetts.

When it began operations in 1999, the pipeline helped shift New England’s power generation away from coal and oil, but it has also created a stronger dependency on fossil gas, leaving citizens vulnerable to price spikes. The region is now planning to accelerate the rollout of renewable energy sources.

The PNGT was not the first fossil fuel infrastructure the BlackRock team behind the Global Infrastructure Fund had snapped up. In a written testimony submitted this March to the State of New Hampshire, a senior executive listed a dozen oil and gas pipelines backed by earlier rounds of the fund. They included one operated by ADNOC, the UAE state-owned oil company whose CEO is Sultan Al-Jaber, COP28 president and chair of ALTÉRRA’s board.

Responding to Climate Home’s findings on where ALTÉRRA’s money is going, Mohamed Adow, director of Nairobi-based think-tank Power Shift Africa, said it is “extremely concerning to see a fund hailed by a COP president as a solution to the climate crisis investing in fossil fuels”.

“This needs to be a wake-up call to the world that these funds created by COP hosts are little more than PR stunts designed to greenwash the activities of fossil fuel-producing nations,” he added.

Oil-backed carbon capture

BlackRock does not disclose the infrastructure fund’s complete portfolio, but it has invested another $550 million in Stratos, the world’s biggest direct air capture (DAC) project being developed in a joint venture with oil giant Occidental. The plant under construction in Texas promises to suck as much as 500,000 tonnes of carbon dioxide out of the atmosphere annually and bury it underground.

Its proponents see DAC as a key technology to balance out emissions in the race to achieve net zero by 2050, although so far it remains expensive and largely unproven at scale. Stratos won a grant from the US government to fast-track the construction of the facility, and it has struck deals to sell carbon offsets generated in future from the plant with corporate giants like Amazon.

Scottish oil-town plan for green jobs sparks climate campers’ anger over local park

When the DAC partnership was announced last November, BlackRock CEO Larry Fink said Stratos “represents an incredible investment opportunity for BlackRock’s clients… and underscores the critical role of American energy companies in climate technology innovation”.

But Stratos’ critics have questioned Occidental’s motivations and dismissed its DAC investments as a greenwashing ploy to keep pumping oil and slow down the transition away from fossil fuels.

“We believe that our direct capture technology is going to be the technology that helps to preserve our industry over time,” Vicki Hollub, Occidental’s chief executive, told the CERAWeek energy industry conference last year. “This gives our industry a license to continue to operate for the 60, 70, 80 years that I think it’s going to be very much needed.”

Call for safeguards

While BlackRock’s infrastructure fund deploys its cash largely in the Global North, ALTÉRRA’s promised investments in developing countries are still taking shape.

Brookfield in June launched a new “Catalytic Transition Fund” backed by ALTÉRRA with a $1-billion commitment. The fund’s stated focus is “directing capital into clean energy and transition assets in emerging economies”.

Climate Home asked ALTÉRRA if it had adopted any exclusion policies that would, for example, rule out investment in certain types of fossil fuels.

The UAE fund did not respond to the question, but a spokesperson said its investment approach is aligned with the goal “of accelerating the climate transition, with a focus on clean energy, industry decarbonization, sustainable living, and climate technologies”.

Climate activists protest against fossil fuels during COP28 in Dubai in December 2023. REUTERS/Thomas Mukoya

350.org’s Sieber called on Al-Jaber – who was widely criticised by green groups for his dual role as president of COP28 and head of a fossil fuel corporation – to “act swiftly to enforce stringent safeguards” for ALTÉRRA’s investments.

“The UAE is on the brink of losing the little credibility it still has left in addressing the urgency of the climate emergency,” Sieber added. “The world, especially communities who are being hit the hardest by climate impacts every day, cannot afford to have one more cent invested in fossil fuels.”

The key question now is whether Azerbaijan – the host of COP29 and itself a substantial producer and exporter of oil and gas – will do things differently. Last week, it announced a new voluntary fund that it said will invest at least $1 billion for emissions reduction projects in developing countries. Baku is hoping to secure contributions for it from fossil-fuel producing nations and companies.

Power Shift Africa’s Adow said developing countries need state-backed climate finance from rich nations, negotiated through the UN climate process, and “not just cooked up in voluntary schemes”. That funding “can be used where the need is greatest, not just where it might make most money for some private profit-seeking businesses,” he added.

(Reporting by Matteo Civillini; fact-checking by Sebastián Rodríguez; editing by Megan Rowling and Sebastián Rodríguez)